When Anne Boden set up fintech upstart Starling Bank from scratch, following the 2008 financial crash, she perhaps wasn’t so ready for how hard it’d be to access funding.

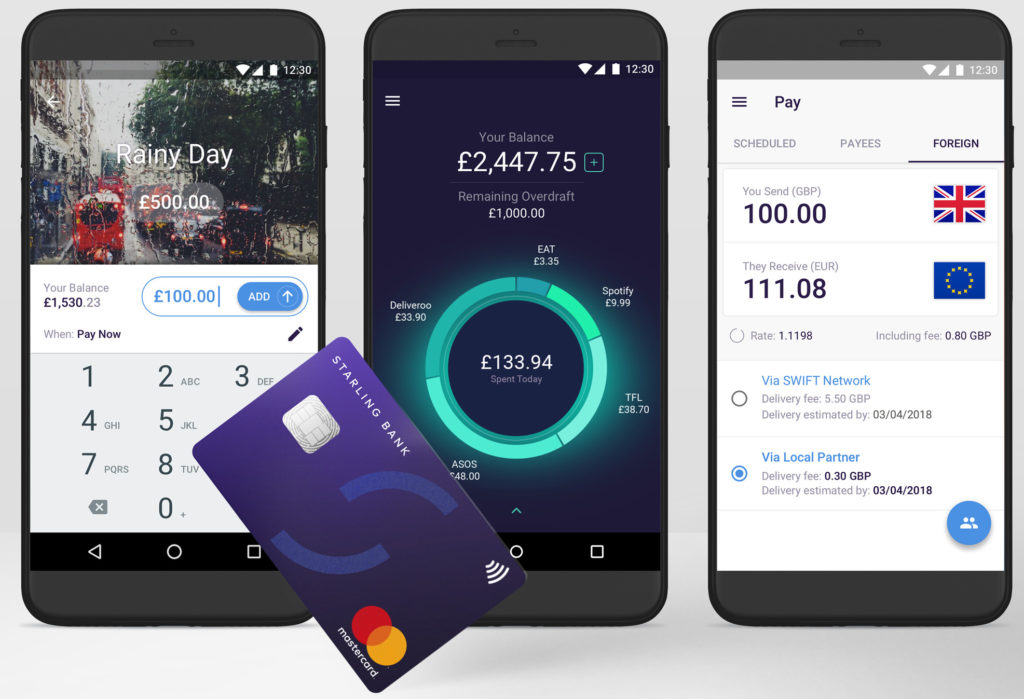

Starling Bank is a mobile-only bank and wants to make it easier for people to manage their money. So far, Starling is a growing business with over 100,000 customers and it recently won British Bank of the year 2018. In a call to GrowthBusiness, Boden is in a jovial mood, following new integrations with Plum, Google Pay and the launch of its joint bank accounts.

Yet following the economic downturn when UK banks became public enemy number one, how did the bank bootstrap itself into success?

‘One of the interesting things about fintech fundraising and the startup scene is a majority of funds will not work with banks,’ she says bluntly. ‘There are rules which means funds backed by British business banks cannot invest in banks.

‘Also, you can’t get any tax relief on your investment in a bank. This also rules out the use of most accelerators which are backed by Government and EIS.’

Ann Boden, CEO of Starling Bank, who founded Starling in 2013 says, ‘When I started the business I couldn’t access any of these Government or EIS funds. So I funded it myself with the help of contingent fees by consultancy firms as traditional schemes such as venture capital and angel investments were simply not available to me.’

Two year wait for funding

So Boden had to be patient when it came to raising the necessary capital to launch the bank and invest in staff and IT systems that were crucial.

‘It wasn’t until two years in when I had progressed the license application a long way and had got into a situation when we knew we would get a banking license that more money came in. We then received £48 million from hedge fund manager Harold McPike, who now owns over 50 per cent of the venture.’

In an interview with GrowthBusiness, Starling rival Atom Bank said it had raised money by Spanish bank BBVA and a number of business people in the North of England.

See more:

FitBit Pay: a UK first from Starling Bank

Interview: David McCarthy, CFO at Atom Bank

How banking finance works

Boden explains what sort of capital you need before you set up a bank.

‘You need long-term capital; capital for operating losses and regulated capital and you need that regulated capital to support your lending. For every £100 million you lend you need about 10-15 per cent in capital.’

Bank capital is when the regulators look at what lending you’re doing to different categories of borrower and they convert this into assets. All your lending to borrowers are assets and regulators add this up into link rated assets. A certain percentage of around eight per cent (this varies depending on the business) of capital have to go into regulated assets and you need capital to support this lending.

‘Liquidity is all about the deposits you take and the lending and the ratios. Capital is how much of your own fund is provided by shareholders which covers your losses. You could have billions of deposits but only millions of capital.’

RBS Remedy Fund to boost Starling

Boden is confident that Starling can access £120 million from the £750 million RBS remedy fund, set up in 2008 to level the playing field in British banking. The fund, which is only available to banks not the entire fintech sector, is divided into two buckets of £450 million given out into tranches, yet nothing so far has been given out.

‘We’ll use this money for marketing and operating costs but we can’t use it for regulatory capital,’ Boden says. ‘We are a fintech that’s also a bank.’

European fintech companies are flush with cash currently and raised $933 million in the first quarter of 2018, according to a report from CBS Insights.

‘Fintech is very attractive at present because the market is dramatically changing. The tech, such as Amazon Web Services that we use, is now available and is resilient. The regulators are allowing new banks and people have changed… they want to use their smartphones for everything.’

Boden is diplomatic when commenting on rival Monzo who saw its losses quadruple from £7.9 million to £33.1 million for the year to February 2018.

‘They (Monzo) have a different model to us and they built up hundreds of thousands of users but pre-paid cards that they use are very expensive.’

Related Stories

Entrepreneurs

5 of the most exciting tech companies in Cardiff

Entrepreneurs

7 easy techniques to remember anything

Entrepreneurs

The 10 most important habits of successful entrepreneurs

Entrepreneurs