Since launching in 1995, AIM has given smaller companies the chance to raise money from institutional investors on the London Stock Exchange (LSE). Over 3,700 companies, including ASOS, Hotel Chocolat and Fever Tree have since listed on AIM and raised over £108 billion in capital in the process.Here, CEO of AIM, Marcus Stuttard, discusses the risks and rewards of floating a business on the AIM market.

When is AIM used in the scaleup cycle?

We see the capital markets, whether that’s AIM or the main market, as being towards the top of the overall funding ladder—without which the earlier stages tend not to work as well. That’s because whether you’re seeking funds from friends, family, an angel or a VC, each are more likely to invest if they can see a range of exit options—from trade sale, handover to another VC or an IPO.

One of the great strengths of AIM is that it’s very diverse. We’ve got companies valued from tens of millions, up to companies like ASOS—valued at over £5 billion. We continue to see some early-stage businesses that might be very capital hungry—often for example the biotechs or technology companies that need funding early on or who need repeat access.

But, we’ve also seen very mature businesses coming through, including those that are family owned— AB Dynamics is a great example of a company where the founder was getting towards retirement and had received offers for the business but floated it at a valuation of £14 million. Rather than selling up, he decided to IPO—it’s now valued at around £200 million.

This is representative of a broader trend: companies coming to the market tend to be that bit bigger and raising a little bit more money. That’s partly a reflection of a much deeper pool of institutional capital that now supports the market. We’re not by design trying to make it more of a mid-cap market but we are interested in creating an easier funding environment for scaleups across the spectrum. And, if there are better, more diverse, funding options at an earlier stage—the companies that then come through to AIM will naturally be that bit bigger.

Have the reasons for floating changed over the last two decades?

Clearly, one of the key reasons that businesses consider an IPO, whether it’s on AIM or any of the markets, is access to capital. In the 23 years since it was launched, over £108 billion has been raised which, for a growth market, we’re very proud of. What we’re equally proud of is the fact that about 65 per cent of that money has been raised by AIM companies after they were admitted to the market—by raising further capital rounds. Many other growth markets support companies that IPO, but don’t have that depth of follow-on capital that now exists behind AIM.

This year, we do see a continuation of that trend. Of the £2 billion that has been raised so far this year; £1.8 billion of that had been raised by companies on the market. Similarly, last year, of the £7 billion raised, £5 billion was through further issues. AIM absolutely provides that long-term repeat access to capital, at a very, very competitive rate.

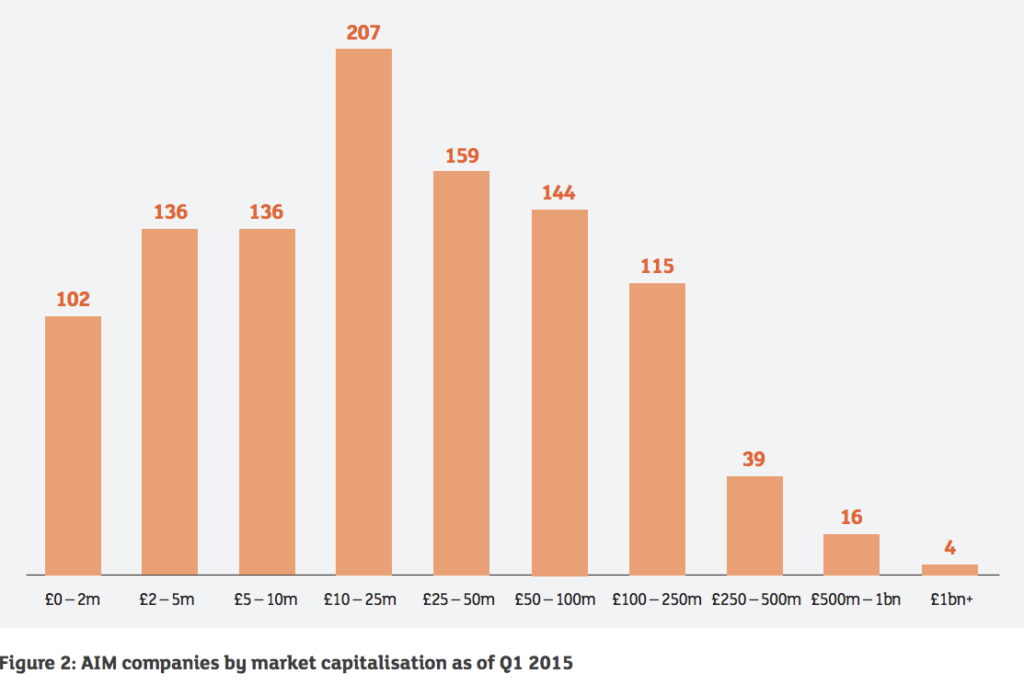

The graph below shows the market cap of companies listed on AIM.

But there are many other benefits of IPO, some of which are lesser known. Many companies, having gone through the IPO process, report being better structured with an enriched management team with a tighter grip over the business and a greater ability to forecast and plan the future.

Indeed, many essential processes of an IPO help the business as a whole. Honing the core equity or growth story, for example, not only attracts investors but brings a company’s proposition into crisper focus, making it easier to explain to employees, suppliers and prospects.

What’s more, IPO brings companies a much higher profile, and, with that, credibility. Knowing that a firm has access to long-term capital can make them a more compelling business partner than their private company peers. I’ve heard of companies that have been able to secure contracts as an AIM company that they couldn’t secure as a private business. And, once you’ve got a publicly traded share, you can use those shares to make acquisitions or incentivise members of your staff with share options that are valued on a real-time basis.

See more:

What does going public on AIM mean for SMEs?

Cake Box to float on AIM stock market

Can the first ever e-cigarette listing on AIM shake up the market?

Is there a perception problem around IPOs?

A common misconception is that, by going public, somehow founders and the management team might lose control over the day-to-day running of the business. The reality for many companies is that having a wide register of investors which can either build their stake or reduce it patiently through the markets, can be a more attractive option than having to formally sell or possibly take a strategic investor that also has a seat on the board.

It can enable a founder to take a bit of capital off the table, so they’ve been able to pay off the mortgage, or put a bit of money in the bank. But, they’ve still held a grip—on the development and future growth of the business.

This article was originally published on business community club The Supper Club

Related Stories

Company Flotations

Cash shells are becoming the hot way to IPO

Company Flotations

The IPO experts

Company Flotations

Float or sink

Company Flotations