When the Alternative Investment Market was launched in 1995 it presented the opportunity for smaller businesses to float shares in a less regulated environment and secure much-needed capital for growth.

However, bringing a business into the public gaze is a double-edged sword: it paves the way for investors to plough money into the company but also makes any failures painfully visible. Nonetheless, AIM’s recent pains seem to be abating.

In the first eight months of 2011 new admissions are up 7 per cent over the same period last year, with 61 new companies joining the junior market (see Table 1 below).

Despite the amount initially raised by these new issues being slightly down, from £548.9 million to £504.2 million, the amount of businesses leaving has fallen by 21 per cent to 99.

The most encouraging development of all is the dramatic rise in acquisitions made by AIM-listed companies, a surge of 51 per cent to 157 transactions (see Table 1 above), proving that the public sphere is providing businesses with much-needed capital ammunition to pursue their M&A growth strategy.

The ability to access fresh funds to target business acquisitions is the reason that Cambridge-based location-tracking company Ubisense took the plunge, in a move that CEO Richard Green described as ‘always part of the plan’.

London Calling

Green explains: ‘I had always had in mind that at some point in the growth of the business we would want access to capital markets of some description, and we got to a point where we thought a London market was a very logical choice.’

Despite the turbulent time that Ubisense decided to list in, Green says that he was overjoyed with the results, with the June listing oversubscribed and providing the business with a market cap of £38.6 million.

Green explains that Ubisense was led through a pre-IPO round which acted as on ‘on-ramp’ to the eventual listing on AIM.

‘The feedback which we got from investors wanting to come in was that we had a very solid story to tell: a great bit of technology with global ambition, and we just needed access to capital to allow us to achieve those ambitions,’ he adds.

People are betting on potential when a business comes to market, Green explains, with the ability to prove that previous growth can be achieved being a huge benefit.

Green adds: ‘It’s not like being in the consumer market, which is very fickle and changes its mind very quickly. Selling to the kind of companies which we do, such as Aston Martin, Mini and Airbus, makes it very easy to track as the lifespans of their products are fairly long, and the production cycles are similarly fairly protracted.’

While Ubisense is under ten years old, the growth markets also offer the opportunity for more established businesses to get in the ring.

Logical Thinking

Water dispensing company Waterlogic had 20 years of solid trading behind them before they made the recent decision to join the junior market.

CEO Jeremy Ben-David says a number of factors motivated the listing, with the desire to make further acquisitions, commercialise new technologies and invest further in manufacturing facilities leading the way.

Ben-David explains: ‘We have a new technology called Firewall, which we developed initially for the business-to-business offering that we already have. However, we realised that we were on to something and saw an opportunity to commercialise it in different areas including the business-to-consumer market.’

The private equity route was one which Ben-David admits crossed his mind. But, on consideration, he felt that AIM offered the right structure for the business going forward.

Getting the IPO to take-off in challenging times was hard work, Ben-David adds, with the performance of other similar ventures looming large in the rear-view mirror.

‘While we were on the roadshow we kept looking at the headlines and seeing 90 per cent of IPOs pulled,’ he comments.

‘Someone once told me that you can float when the market is good and when the market is bad, but the real challenge is floating when there is a bit of volatility, which is of course what we experienced.’

Ben-David attributes the strong investor interest which Waterlogic received to the fact that it was a good ongoing business, with an aspect of new technology and a track record of recurring revenues. The listing was two and a half times over-subscribed – a great result, he adds.

The hardest aspect of the IPO was leaving the day-to-day running of the business for six months, Ben-David believes. ‘No matter what anyone tells you, an IPO is not something that you can do at the same time as you are doing your day job.’

Despite the attention that Ben-David and chief financial officer Steve Harrison had to pay to the listing, Waterlogic’s management team still managed to land three acquisitions during the period, taking the deal count to 19 during the company’s history.

Having completed the move to the public market, Ben-David hopes the move will provide Waterlogic with a little ‘kudos’ when it comes to making further acquisitions, with AIM giving Waterlogic the currency it needs to get deals done.

Risky Business

Waterlogic succeeded in part becuase it was an extablished business with a good track record was an established business with a good track record. New businesses aren’t received with such open arms by investors, says managing director of MAM Funds, Gervais Williams.

‘Investors are starting to move towards areas which are less volatile. The nice thing about an oil and gas stock is that if you get it right you can make five times your money, but the unfortunate thing is that if you get it wrong you can loose four-fifths of your money,’ Williams explains.

New companies coming to market are finding it very hard to convince an investor that they should sell an existing investment which they know, even if it is not trading as well as they hope, and move into a new investment, Williams adds.

For businesses that appear to be struggling, Williams is adamant that a delisting is not the best option. ‘If you have gone through all the costs of becoming a PLC, even if your share price has come down a long way from the issue price because of the recession, I think the advantage of a listing is huge.’

Williams sees smaller companies as the best-performing sector in the next five years, with trends starting to move in their favour, even if they haven’t actually realised yet.

The risk-averse nature of today’s investors is mirrored by Williams’s own recently raised fund, The Diverse Income Trust, which is only two thirds invested from the initial £50 million raised back in March.

Looking forward into an uncertain and ‘murky’ market, it is the ability to raise capital which will be absolutely paramount for businesses, says Williams, with those that already have a listing at a distinct advantage.

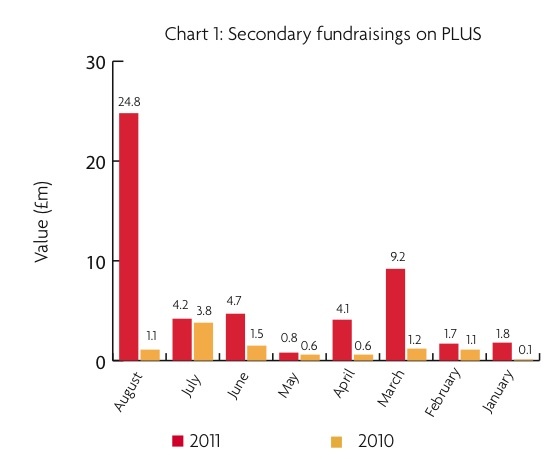

Over on PLUS SX, secondary fundraisings during the first eight months of 2011 reached £51.3 million, up substantially from the £10.1 million posted during the same period in 2010 (see Chart 1 below). With delistings down 15 per cent and new admissions up 29 per cent, Vivienne Cassley, of PLUS Markets Group, argues that the indicators are looking good.

‘Trading has been strong, which I think is a good sign. Through the first quarter of the year, trading in our own PLUS companies was up 130 per cent over the same period last year.’

Related Stories

Company Flotations

Cash shells are becoming the hot way to IPO

Company Flotations

The IPO experts

Company Flotations

Float or sink

Company Flotations